Python for Stock Market Analysis: Getting Started into Modeling Timeseries

Introduction

Hello there, this is the part 5 of Python for Stock Market Analysis and in this part, we will continue from where we left i.e. modeling a timeseries. Finding a best set of parameters that gives highly accurate prediction is always a hard job and there is not always a guarantee that one can find the best parameters. There are few reasons due to which we can not find best parameters of timeseries model:

- Series can be resembling white noise.

- Series can be random walk.

- External variables (Exogenous) could be in action.

But with assuming that we are ready to break above problems, lets get into modeling.

import pandas as pd

import plotly.express as px

import cufflinks

import plotly.io as pio

import yfinance as yf

import warnings

import matplotlib.pyplot as plt

import seaborn as sns

sns.set()

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

from statsmodels.tsa.arima_model import ARMA, ARIMA

import statsmodels.api as sm

warnings.filterwarnings("ignore")

cufflinks.go_offline()

cufflinks.set_config_file(world_readable=True, theme='pearl')

pio.renderers.default = "notebook" # should change by looking into pio.renderers

sns.set(rc={'figure.figsize':(40, 20)})

plt.rc("figure", figsize=(16,8))

pd.options.display.max_columns = None

symbols = ["AAPL"]

df = yf.download(tickers=symbols,start="2002-02-01")

df.columns = [c.lower() for c in df.columns]

df.rename(columns={"adj close":"adj_close"},inplace=True)

df.head()

NumExpr defaulting to 8 threads.

[*********************100%***********************] 1 of 1 completed

| open | high | low | close | adj_close | volume | |

|---|---|---|---|---|---|---|

| Date | ||||||

| 2002-01-31 | 0.431429 | 0.441607 | 0.430536 | 0.441429 | 0.377984 | 468445600 |

| 2002-02-01 | 0.434643 | 0.445714 | 0.434643 | 0.435893 | 0.373244 | 398305600 |

| 2002-02-04 | 0.434286 | 0.455714 | 0.432143 | 0.452679 | 0.387617 | 522373600 |

| 2002-02-05 | 0.448036 | 0.463929 | 0.447857 | 0.454464 | 0.389146 | 456887200 |

| 2002-02-06 | 0.457143 | 0.463929 | 0.431250 | 0.440536 | 0.377220 | 597576000 |

Metrics

def percentage_change(forecast, actual, threshold=10):

pchange = 100*(forecast-actual)/actual

acc = (pchange.abs()<threshold).sum()/len(pchange)

return acc

def mean_squared(forecast, actual):

return np.mean((forecast - actual)**2)

Auto Regression (AR)

Auto regression is nothing more than a linear relationship of a series with lagged version of itself.

Formula to represent AR model is:

\(x_t = c + \phi.x_{(t-1)} + \epsilon_t\) Where,

- c is constant.

- xt is the current value.

- x_(t-1) is the value of previous period.

- 𝜖𝑡 is the residual value.

If data is from non stationarity process then AR models fails.

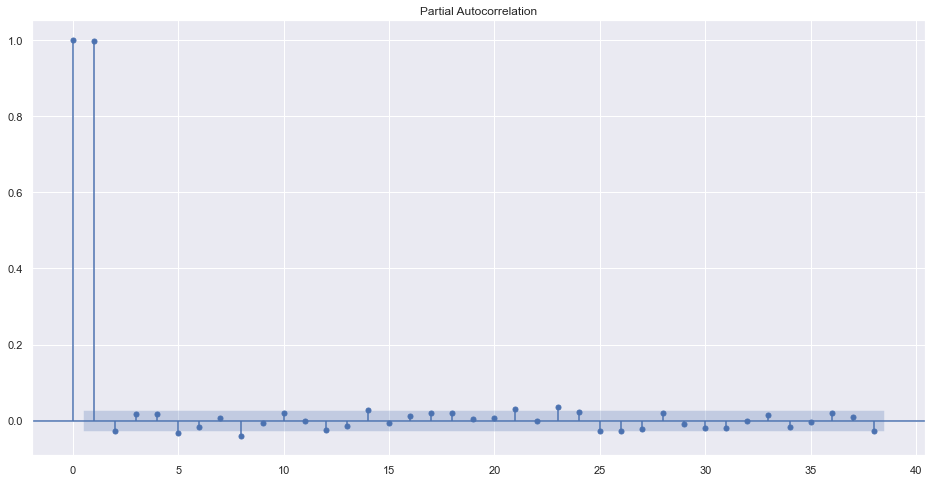

The value of lag should be chosen by examining the PACF plot i.e choose last significant value of lag before it becomes insignificant.

plot_pacf(df.adj_close)

plt.plot()

[]

It seems that after the first lag, the values became insignificant. So the best order of AR can be 1.

LLR Test

To check if two models are significantly different or not. If the p-value is lower than 5%, then we should choose the later model. Always use simpler model at first. The degree of freedom is chosen by subtracting order values.

from scipy.stats.distributions import chi2

def LLR_test(mod1, mod2, degf=1):

l1 = mod1.fit().llf

l2 = mod2.fit().llf

lr = (2*(l2-l1))

p = chi2.sf(lr, degf).round(3)

return p

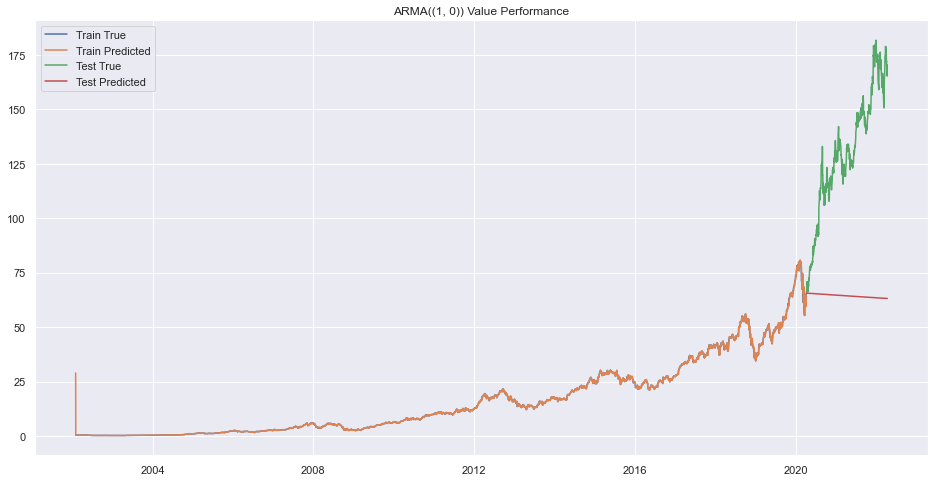

rmodel1 = ARMA(df.adj_close, order=(1, 0))

rresults1 = rmodel1.fit()

print(rresults1.summary())

rmodel3 = ARMA(df.adj_close, order=(2, 0))

rresults3 = rmodel3.fit()

print(rresults3.summary())

LLR_test(rmodel1, rmodel3, 1)

ARMA Model Results

==============================================================================

Dep. Variable: adj_close No. Observations: 5088

Model: ARMA(1, 0) Log Likelihood -6715.633

Method: css-mle S.D. of innovations 0.904

Date: Sat, 16 Apr 2022 AIC 13437.266

Time: 12:59:22 BIC 13456.870

Sample: 0 HQIC 13444.131

===================================================================================

coef std err z P>|z| [0.025 0.975]

-----------------------------------------------------------------------------------

const 27.7966 nan nan nan nan nan

ar.L1.adj_close 1.0000 nan nan nan nan nan

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 1.0000 +0.0000j 1.0000 0.0000

-----------------------------------------------------------------------------

ARMA Model Results

==============================================================================

Dep. Variable: adj_close No. Observations: 5088

Model: ARMA(2, 0) Log Likelihood -6712.381

Method: css-mle S.D. of innovations 0.903

Date: Sat, 16 Apr 2022 AIC 13432.761

Time: 12:59:22 BIC 13458.900

Sample: 0 HQIC 13441.914

===================================================================================

coef std err z P>|z| [0.025 0.975]

-----------------------------------------------------------------------------------

const 27.7475 nan nan nan nan nan

ar.L1.adj_close 0.9611 7.05e-06 1.36e+05 0.000 0.961 0.961

ar.L2.adj_close 0.0389 7.33e-07 5.31e+04 0.000 0.039 0.039

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 1.0000 +0.0000j 1.0000 0.0000

AR.2 -25.6971 +0.0000j 25.6971 0.5000

-----------------------------------------------------------------------------

0.011

It seems that the model with order 2 is slightly more significant than of order 1. But lets check with 3rd order and second.

rmodel1 = ARMA(df.adj_close, order=(2, 0))

rresults1 = rmodel1.fit()

print(rresults1.summary())

rmodel3 = ARMA(df.adj_close, order=(3, 0))

rresults3 = rmodel3.fit()

print(rresults3.summary())

LLR_test(rmodel1, rmodel3, 1)

ARMA Model Results

==============================================================================

Dep. Variable: adj_close No. Observations: 5088

Model: ARMA(2, 0) Log Likelihood -6712.381

Method: css-mle S.D. of innovations 0.903

Date: Sat, 16 Apr 2022 AIC 13432.761

Time: 12:59:24 BIC 13458.900

Sample: 0 HQIC 13441.914

===================================================================================

coef std err z P>|z| [0.025 0.975]

-----------------------------------------------------------------------------------

const 27.7475 nan nan nan nan nan

ar.L1.adj_close 0.9611 7.05e-06 1.36e+05 0.000 0.961 0.961

ar.L2.adj_close 0.0389 7.33e-07 5.31e+04 0.000 0.039 0.039

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 1.0000 +0.0000j 1.0000 0.0000

AR.2 -25.6971 +0.0000j 25.6971 0.5000

-----------------------------------------------------------------------------

ARMA Model Results

==============================================================================

Dep. Variable: adj_close No. Observations: 5088

Model: ARMA(3, 0) Log Likelihood -6711.479

Method: css-mle S.D. of innovations 0.903

Date: Sat, 16 Apr 2022 AIC 13432.958

Time: 12:59:26 BIC 13465.631

Sample: 0 HQIC 13444.399

===================================================================================

coef std err z P>|z| [0.025 0.975]

-----------------------------------------------------------------------------------

const 27.7084 nan nan nan nan nan

ar.L1.adj_close 0.9610 7.05e-06 1.36e+05 0.000 0.961 0.961

ar.L2.adj_close 0.0358 0.014 2.565 0.010 0.008 0.063

ar.L3.adj_close 0.0033 0.014 0.234 0.815 -0.024 0.031

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 1.0000 -0.0000j 1.0000 -0.0000

AR.2 -5.9821 -16.4548j 17.5084 -0.3055

AR.3 -5.9821 +16.4548j 17.5084 0.3055

-----------------------------------------------------------------------------

0.179

It is not significant. Thus we will choose the order of 1 or 2. Lets see the result by making a forecasting.

Train/Test Split

from sklearn.model_selection import train_test_split

train, test = train_test_split(df, test_size=0.1, shuffle=False)

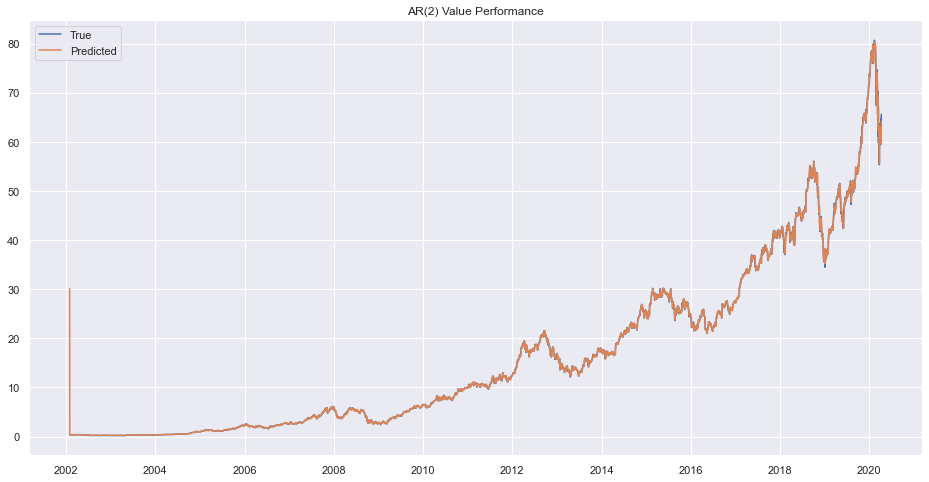

rrmodel1 = ARMA(train.adj_close, order=(2, 0))

rrresults1 = rrmodel1.fit()

# print(rresults1.summary())

# rrresults1.plot_predict(dynamic=False)

# plt.title("AR(2) Model Difference Performance")

# plt.show()

prd = rrresults1.predict()

plt.plot(train.adj_close)

plt.plot(prd)

plt.legend(["True", "Predicted"])

plt.title("AR(2) Value Performance")

plt.show()

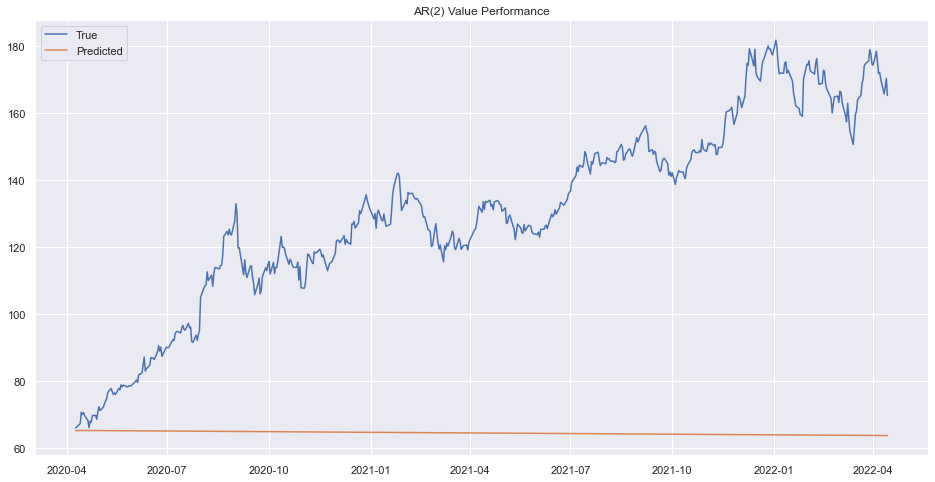

prd=rrresults1.forecast(steps=len(test))[0]

prd = pd.Series(prd, index=test.index)

plt.plot(test.adj_close)

plt.plot(prd)

plt.legend(["True", "Predicted"])

plt.title("AR(2) Value Performance")

plt.show()

Prediction on train set was okay but not in the test set. lets try another order.

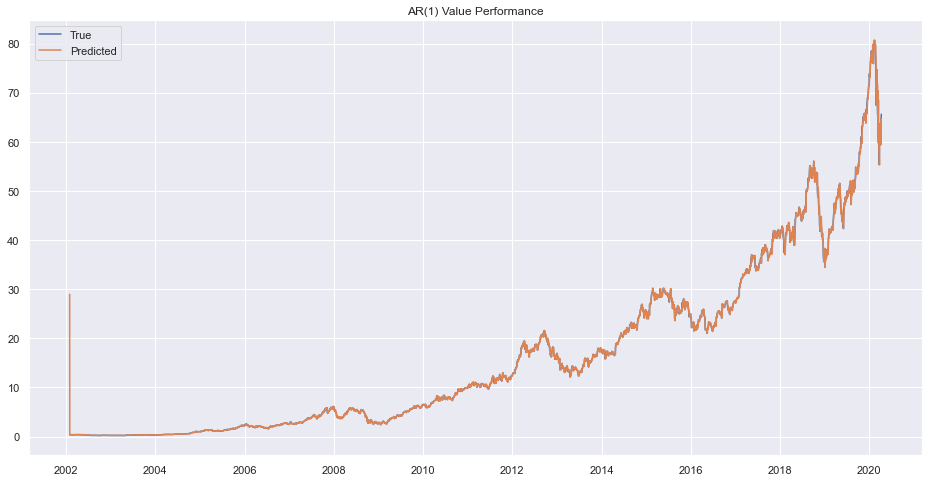

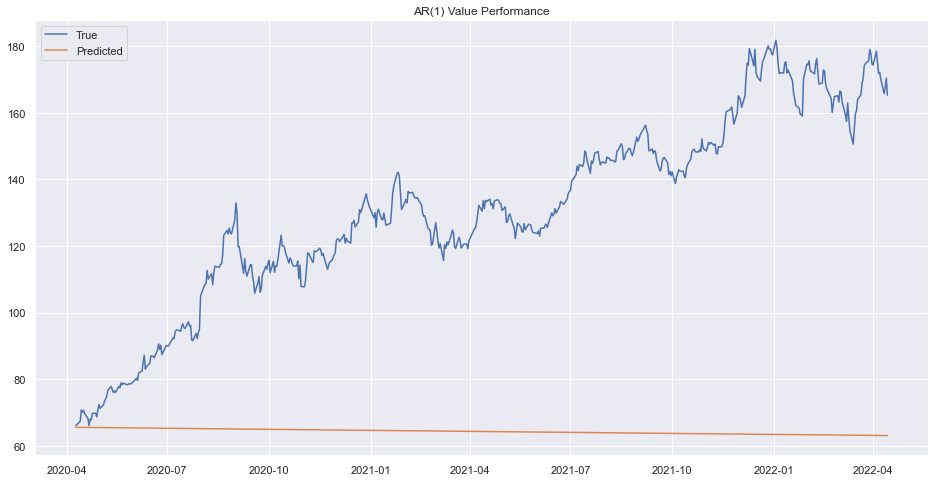

rrmodel1 = ARMA(train.adj_close, order=(1, 0))

rrresults1 = rrmodel1.fit()

prd = rrresults1.predict()

plt.plot(train.adj_close)

plt.plot(prd)

plt.legend(["True", "Predicted"])

plt.title("AR(1) Value Performance")

plt.show()

prd=rrresults1.forecast(steps=len(test))[0]

prd = pd.Series(prd, index=test.index)

plt.plot(test.adj_close)

plt.plot(prd)

plt.legend(["True", "Predicted"])

plt.title("AR(1) Value Performance")

plt.show()

The result is bad. Lets try to find Moving Average Model.

Moving Average (MA)

We have written a good blog about MA in first part of this blog series please refer it for how MA is best idea to look into.

Just like AR model, MA model also uses lag term which is determined using the ACF plot. \(r_t = c + \theta_1.\epsilon_{t-1} + \epsilon_t\) Where,

- rt, is value in current period.

- theta, what part of the error last period is relevant in explaining the current value.

- epsilon, error terms of respective time periods.

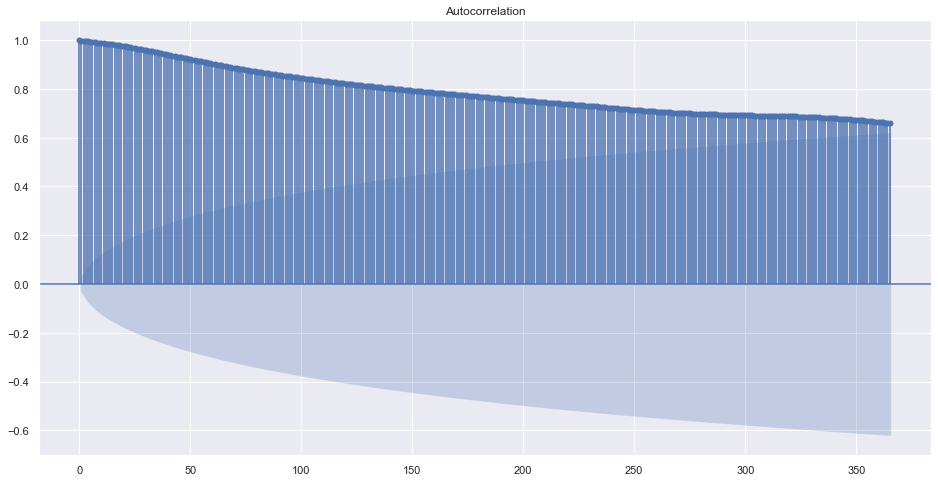

MA(1) is nearly identical to AR(inf). We can find order of MA using ACF plot.

plot_acf(train.adj_close, lags=365)

plt.plot()

[]

The order of MA is hard to find here because there is not a significant changes but slow decrease of correlation. May be because this is a daily data. What happens in a monthly average?

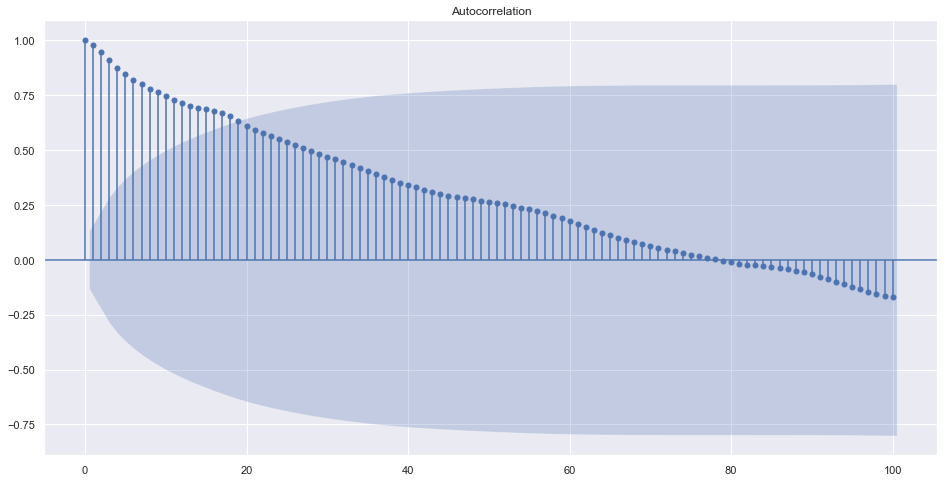

plot_acf(train.resample("1M").adj_close.mean(), lags=100)

plt.plot()

[]

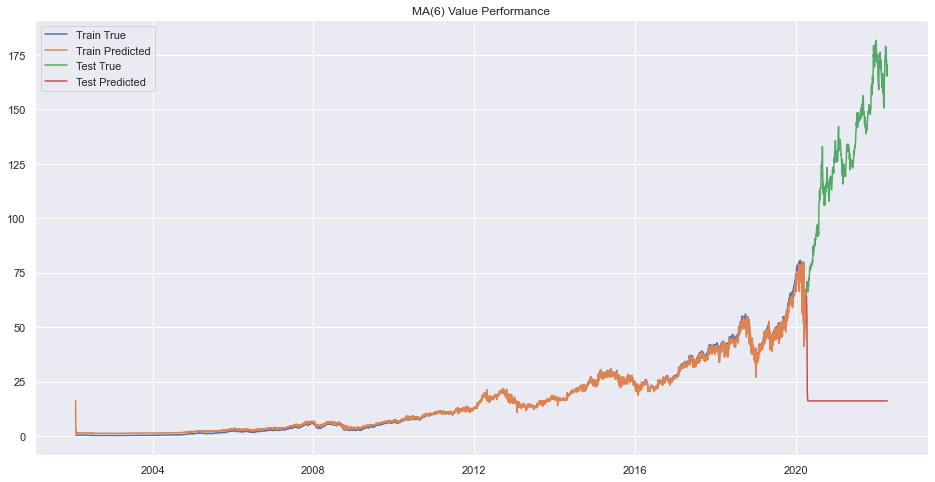

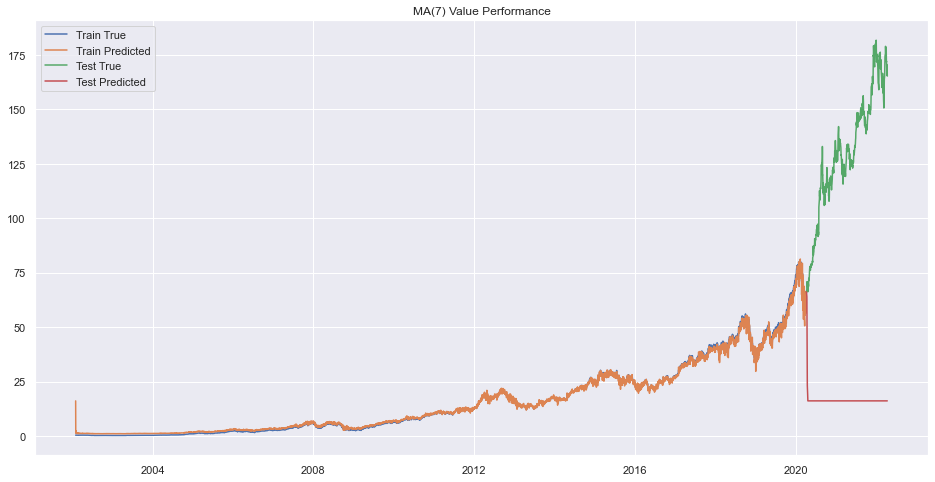

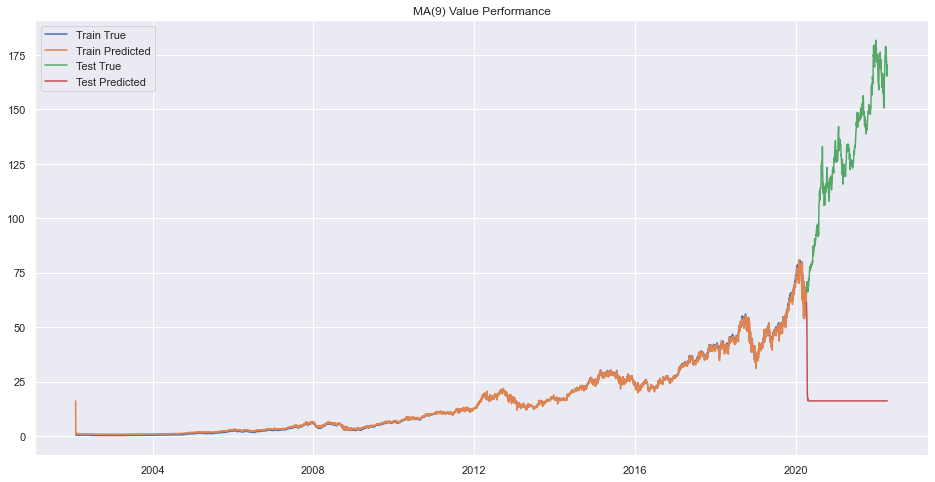

Now we can see that the best order can be below 20 and choices are from 1. ARMA(0,1) is MA(1).

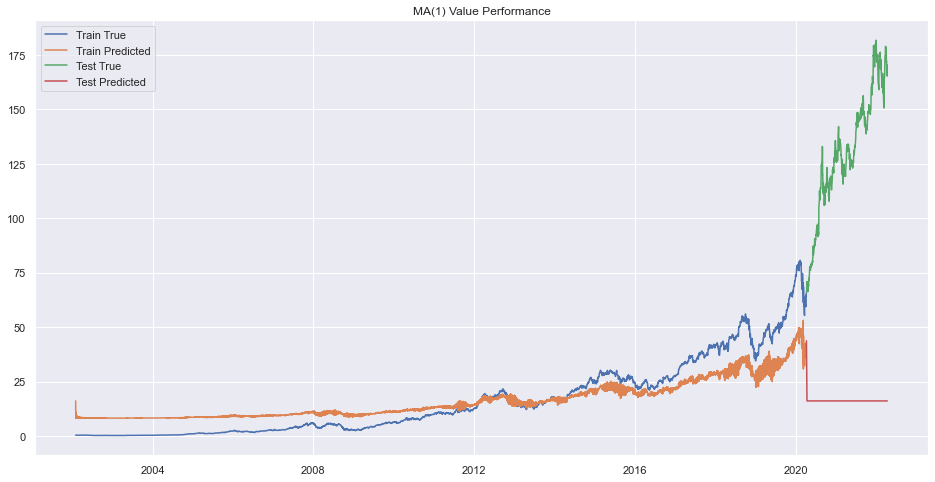

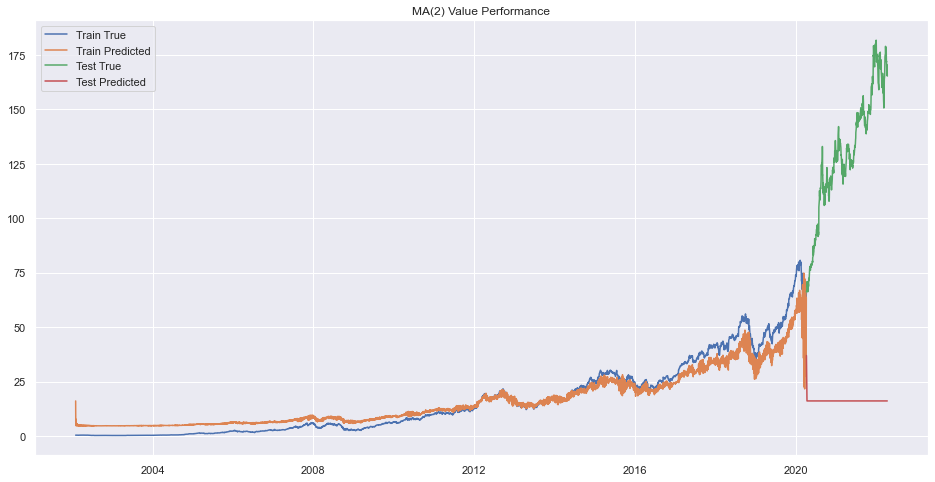

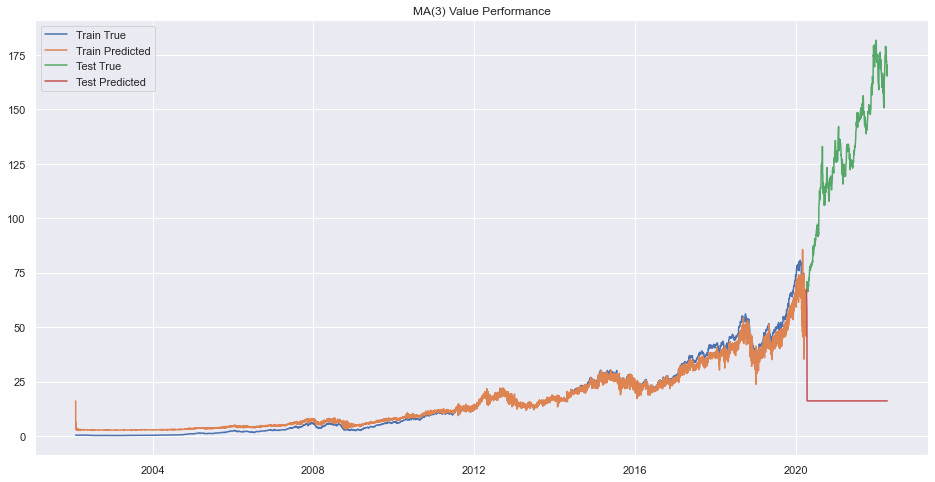

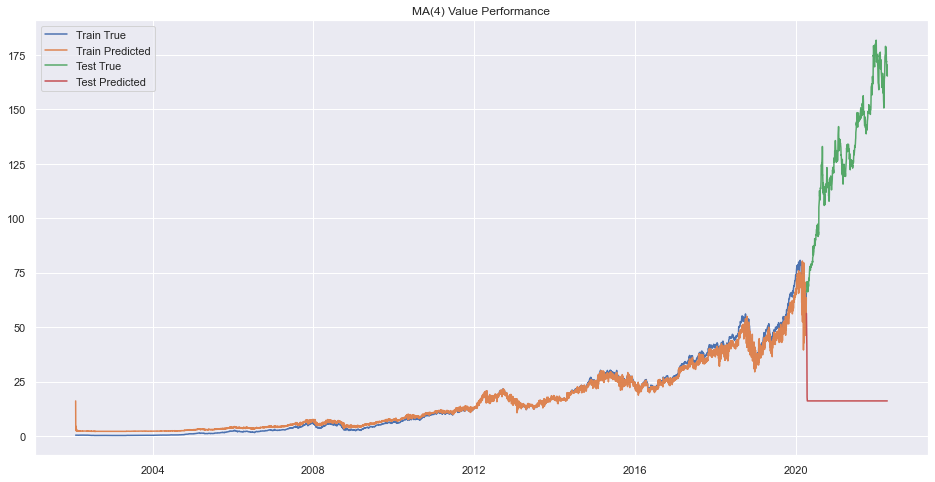

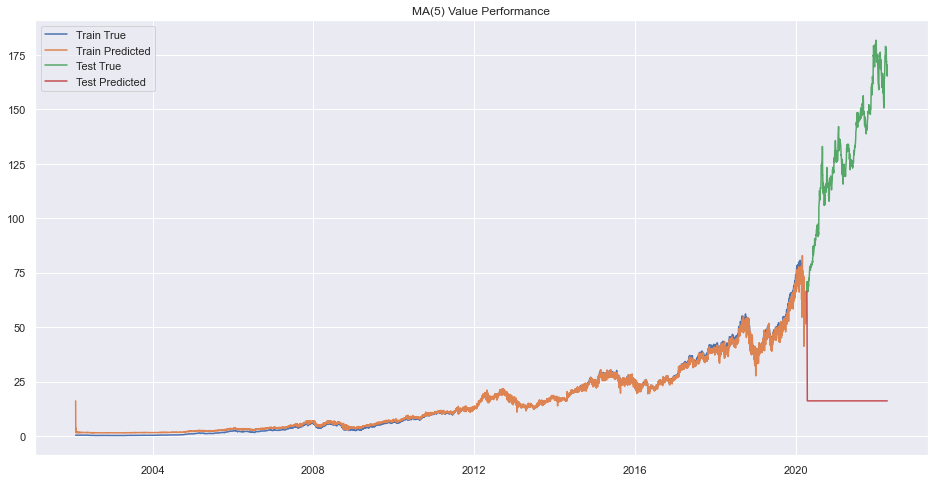

Best MA Model

best=None

pq = 0

for q in range(1,10):

try:

model1 = ARMA(train.adj_close, order=(0, q))

rrresults1 = model1.fit()

if best is None:

best=model1

pq=q

else:

if LLR_test(best, model1, q-pq)<0.05:

best=model1

pq=q

prd = rrresults1.predict()

plt.plot(train.adj_close)

plt.plot(prd)

prd=rrresults1.forecast(steps=len(test))[0]

prd = pd.Series(prd, index=test.index)

plt.plot(test.adj_close)

plt.plot(prd)

plt.legend(["Train True", "Train Predicted", "Test True", "Test Predicted"])

plt.title(f"MA({q}) Value Performance")

plt.show()

except:

print(f"Error on order {q}")

Error on order 8

print(f"Best Order is {pq}.")

Best Order is 9.

There seems to be very bad forecasting but performance on train data was okay.

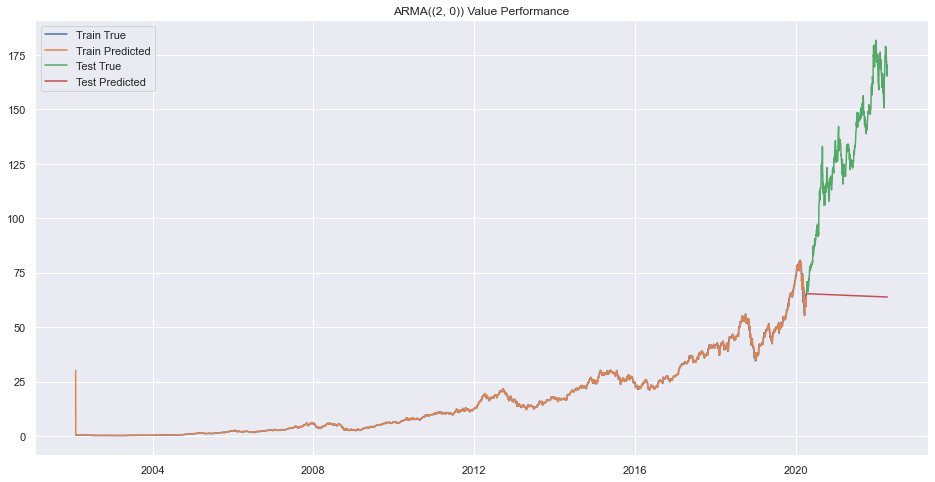

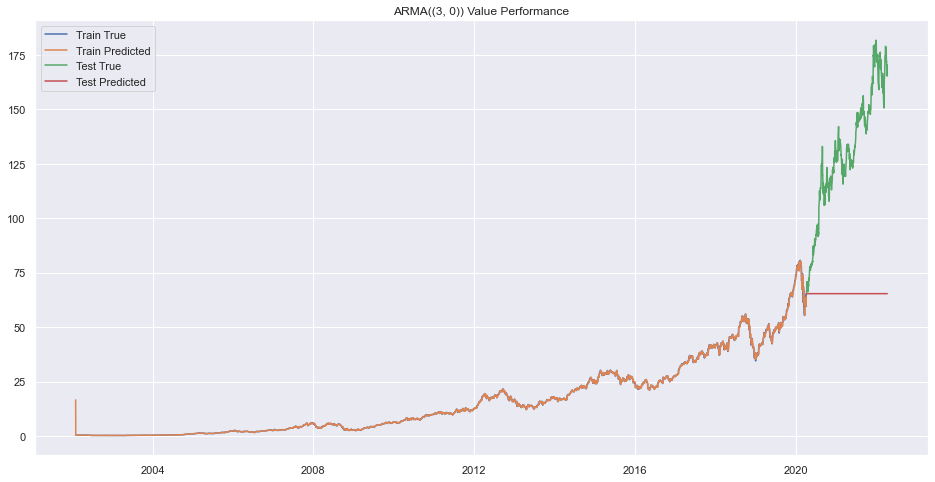

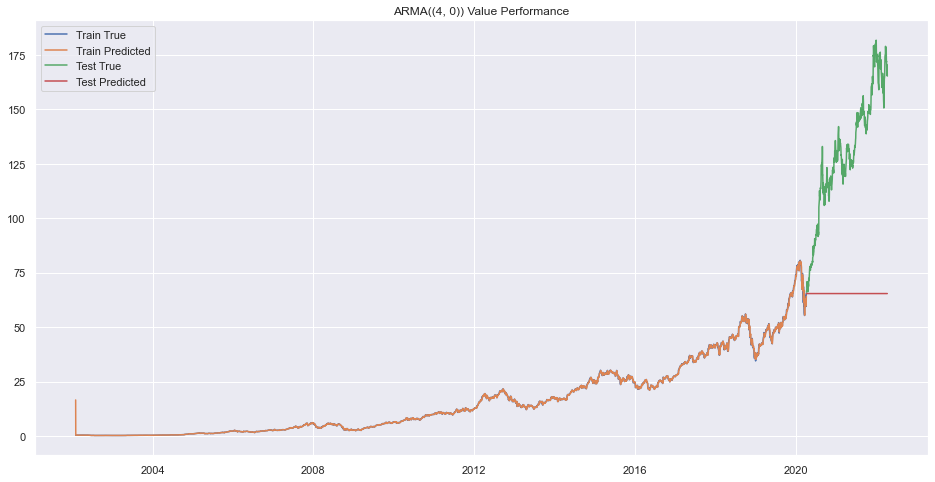

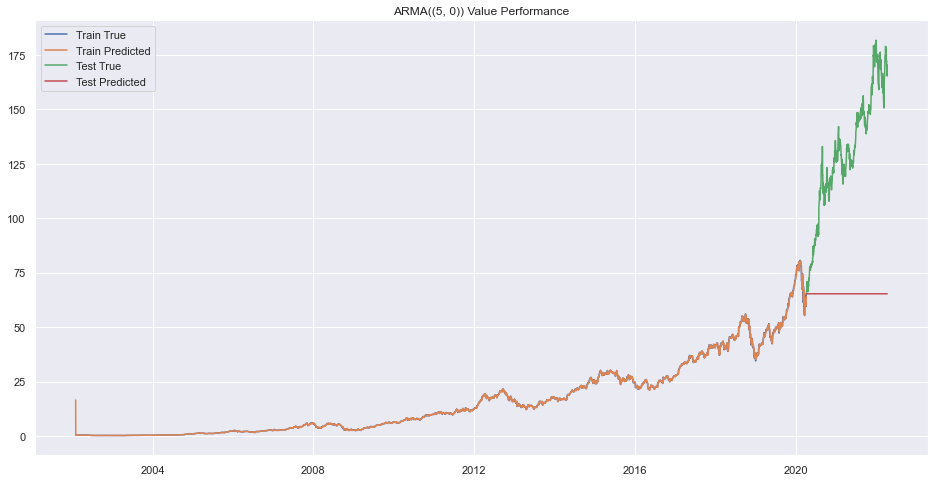

Auto Regression and Moving Average (ARMA)

It is simple a sum of AR and MA model.

ARMA=AR+MA

Finding Best Orders

best=None

pq = 0

pp = 0

for p in range(1,10):

for q in range(10):

try:

model1 = ARMA(train.adj_close, order=(p, q))

rrresults1 = model1.fit()

if best is None:

best=model1

pq=q

pp = p

else:

if LLR_test(best, model1, q-pq)<0.05:

best=model1

pq=q

pp=p

prd = rrresults1.predict()

plt.plot(train.adj_close)

plt.plot(prd)

prd=rrresults1.forecast(steps=len(test))[0]

prd = pd.Series(prd, index=test.index)

plt.plot(test.adj_close)

plt.plot(prd)

plt.legend(["Train True", "Train Predicted", "Test True", "Test Predicted"])

plt.title(f"ARMA({(p,q)}) Value Performance")

plt.show()

except Exception as e:

# raise e

print(f"Error on order {(p,q)}")

Error on order (1, 1)

Error on order (1, 2)

Error on order (1, 3)

Error on order (1, 4)

Error on order (1, 5)

Error on order (1, 6)

Error on order (1, 7)

Error on order (1, 8)

Error on order (1, 9)

Error on order (2, 1)

Error on order (2, 2)

Error on order (2, 3)

Error on order (2, 4)

Error on order (2, 5)

Error on order (2, 6)

Error on order (2, 7)

Error on order (2, 8)

Error on order (2, 9)

Error on order (3, 1)

Error on order (3, 2)

Error on order (3, 3)

Error on order (3, 4)

Error on order (3, 5)

Error on order (3, 6)

Error on order (3, 7)

Error on order (3, 8)

Error on order (3, 9)

Error on order (4, 1)

Error on order (4, 2)

Error on order (4, 3)

Error on order (4, 4)

Error on order (4, 5)

Error on order (4, 6)

Error on order (4, 7)

Error on order (4, 8)

Error on order (4, 9)

Error on order (5, 1)

Error on order (5, 2)

Error on order (5, 3)

Error on order (5, 4)

Error on order (5, 5)

Error on order (5, 6)

Error on order (5, 7)

Error on order (5, 8)

Error on order (5, 9)

Error on order (6, 1)

Error on order (6, 2)

Error on order (6, 3)

Error on order (6, 4)

Error on order (6, 5)

Error on order (6, 6)

Error on order (6, 7)

Error on order (6, 8)

Error on order (6, 9)

Error on order (7, 1)

Error on order (7, 2)

Error on order (7, 3)

Error on order (7, 4)

Error on order (7, 5)

Error on order (7, 6)

Error on order (7, 7)

Error on order (7, 8)

Error on order (7, 9)

Error on order (8, 1)

Error on order (8, 2)

Error on order (8, 3)

Error on order (8, 4)

Error on order (8, 5)

Error on order (8, 6)

Error on order (8, 7)

Error on order (8, 8)

Error on order (8, 9)

Error on order (9, 1)

Error on order (9, 2)

Error on order (9, 3)

Error on order (9, 4)

Error on order (9, 5)

Error on order (9, 6)

Error on order (9, 7)

Error on order (9, 8)

Error on order (9, 9)

ARIMA

Add integration feature to the ARMA. It has 3 values as order, (p, d, q) p from AR, d as integrating order and q as MA order.

How to find differencing term?

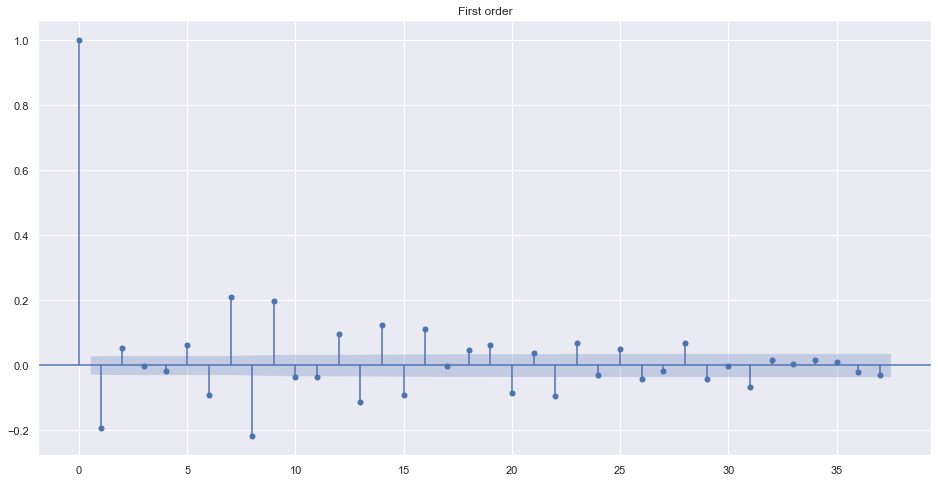

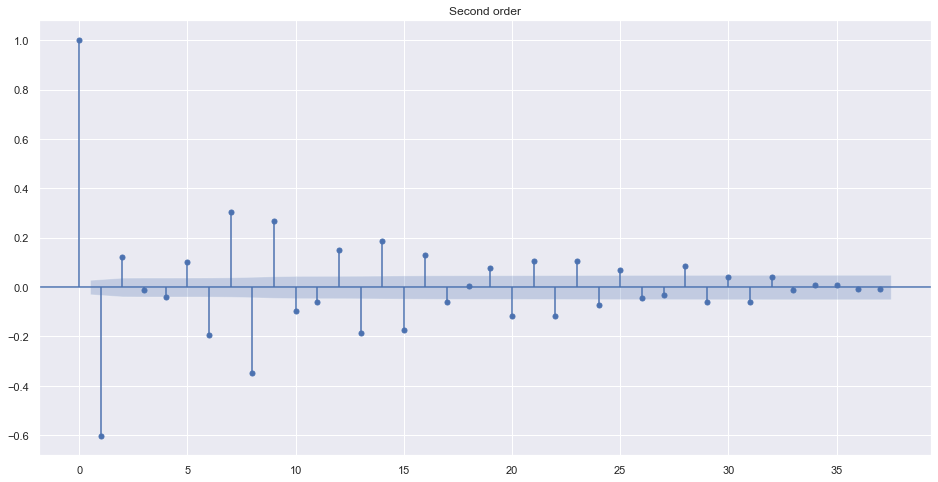

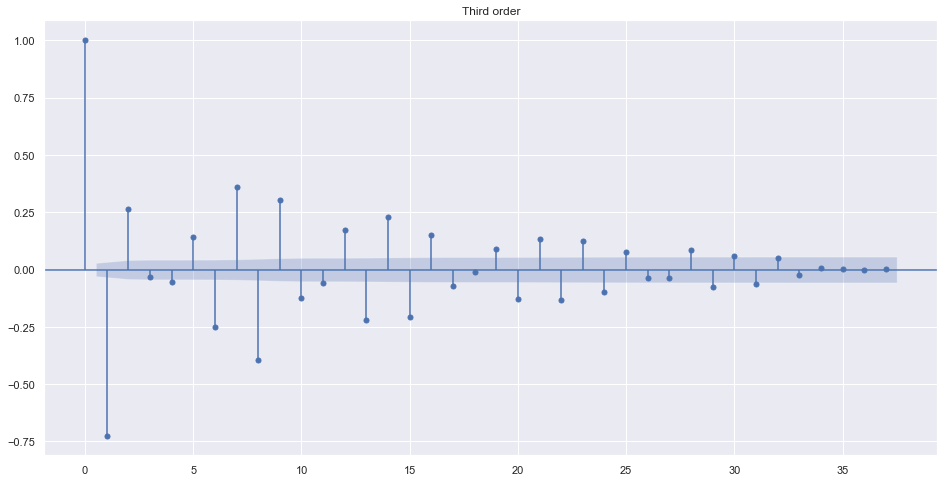

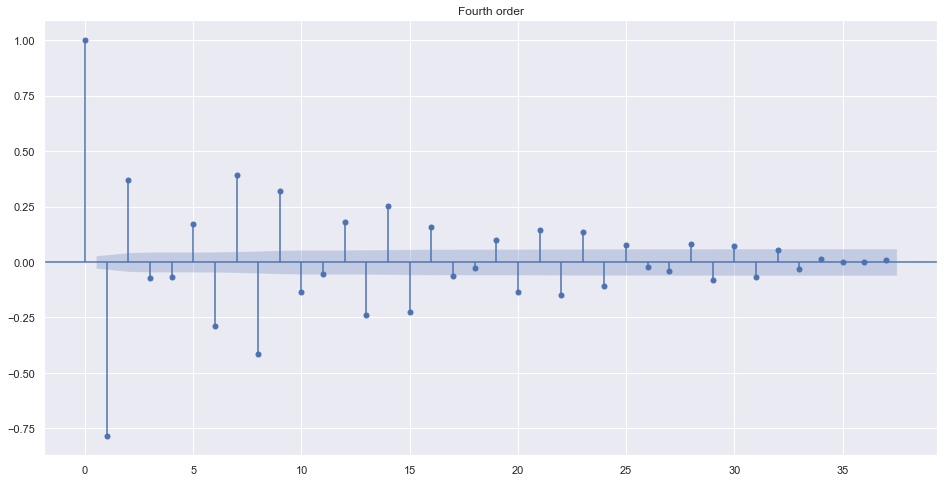

The differencing term is needed only if the data is not stationary. Look at the ACF of different order of value.

plot_acf(train.adj_close.diff().dropna(), title="First order")

plot_acf(train.adj_close.diff().diff().dropna(), title="Second order")

plot_acf(train.adj_close.diff().diff().diff().dropna(), title="Third order")

plot_acf(train.adj_close.diff().diff().diff().diff().dropna(), title="Fourth order")

plt.show()

Alternatively, we can find best order by looking into ndiffs from pmdarima. It uses different algorithms to make data stationary.

from pmdarima.arima.utils import ndiffs

# adf

print(ndiffs(train.adj_close, test='adf') )

# KPSS test

print(ndiffs(train.adj_close, test='kpss') )

# PP test:

print(ndiffs(train.adj_close, test='pp') )

1

1

1

Grid Search

We will find best order of p,d,q in ARIMA(p,d,q) using GridSearch by manually trying each order and taking the best model as that which have very little AIC (Akaike Information Criterion).

from statsmodels.tsa.arima_model import ARIMA

import numpy as np

best_aic = np.inf

best_order = None

best_mdl = None

pq_rng = range(5)

d_rng = range(3)

for i in pq_rng:

for d in d_rng:

for j in pq_rng:

try:

tmp_mdl = ARIMA(train.adj_close, order=(i,d,j)).fit(method='mle', trend='nc')

tmp_aic = tmp_mdl.aic

print(f"Order: {(i, d, j)} AIC: {tmp_aic}")

if tmp_aic < best_aic:

best_aic = tmp_aic

best_order = (i, d, j)

best_mdl = tmp_mdl

except: continue

print('aic: {:6.5f} | order: {}'.format(best_aic, best_order))

Order: (0, 0, 1) AIC: 35649.957536726

Order: (0, 0, 2) AIC: 30452.926279850846

Order: (0, 0, 3) AIC: 25568.02974006658

Order: (0, 0, 4) AIC: 23135.908151069194

Order: (0, 1, 1) AIC: 6113.786234527973

Order: (0, 1, 2) AIC: 6103.676229595621

Order: (0, 1, 3) AIC: 6105.164302350337

Order: (0, 1, 4) AIC: 6107.097404802813

Order: (0, 2, 1) AIC: 6279.333482578022

Order: (0, 2, 2) AIC: 6116.57706331723

Order: (0, 2, 3) AIC: 6107.231252247981

Order: (0, 2, 4) AIC: 6108.574009581484

Order: (1, 0, 0) AIC: 6286.055625234081

Order: (1, 1, 0) AIC: 6102.620679110958

Order: (1, 1, 1) AIC: 6103.588554384392

Order: (1, 1, 2) AIC: 6062.107525235468

Order: (1, 1, 3) AIC: 6025.035860265804

Order: (1, 1, 4) AIC: 6010.0475679855035

Order: (1, 2, 0) AIC: 8186.521128276045

Order: (1, 2, 1) AIC: 6105.782414442538

Order: (1, 2, 3) AIC: 6064.5909315706185

Order: (1, 2, 4) AIC: 6028.885354842478

Order: (2, 0, 0) AIC: 6114.971431245766

Order: (2, 1, 0) AIC: 6103.477381158474

Order: (2, 1, 1) AIC: 6022.377015689852

Order: (2, 1, 2) AIC: 5760.708197093179

Order: (2, 1, 3) AIC: 5757.064480023204

Order: (2, 1, 4) AIC: 5730.498097448992

Order: (2, 2, 0) AIC: 7494.63308055631

Order: (2, 2, 1) AIC: 6106.877059300763

Order: (2, 2, 2) AIC: 6024.98016765312

Order: (2, 2, 3) AIC: 5765.884270710813

Order: (2, 2, 4) AIC: 5761.035898560531

Order: (3, 0, 0) AIC: 6115.823336513856

Order: (3, 1, 0) AIC: 6105.167397240131

Order: (3, 1, 1) AIC: 5991.37372259965

Order: (3, 1, 2) AIC: 5758.0483590846325

Order: (3, 1, 3) AIC: 5761.908569933521

Order: (3, 1, 4) AIC: 5753.150426707316

Order: (3, 2, 0) AIC: 7197.488347782065

Order: (3, 2, 1) AIC: 6108.672772554836

Order: (3, 2, 2) AIC: 5995.295668276515

Order: (3, 2, 3) AIC: 5762.135834467263

Order: (3, 2, 4) AIC: 5756.864902029758

Order: (4, 0, 0) AIC: 6117.512002741951

Order: (4, 1, 0) AIC: 6105.494823494794

Order: (4, 1, 1) AIC: 5962.014235342666

Order: (4, 1, 2) AIC: 5729.617168795675

Order: (4, 1, 3) AIC: 5755.675520221222

Order: (4, 1, 4) AIC: 5724.10687968731

Order: (4, 2, 0) AIC: 6871.860230500325

Order: (4, 2, 1) AIC: 6108.71314094866

Order: (4, 2, 2) AIC: 5964.708773988523

Order: (4, 2, 3) AIC: 5732.423313869451

Order: (4, 2, 4) AIC: 5736.016922455731

aic: 5724.10688 | order: (4, 1, 4)

fitted = best_mdl.predict(start=best_order[1], end=len(train))

index_of_fc = train.adj_close.index

fseries = pd.Series(fitted, index=index_of_fc)

#plot

plt.figure(figsize=(20, 10), dpi=100)

plt.plot(train.adj_close, label="Train Actual", color="darkgreen")

plt.plot(fseries, label="Train Forecast", color="darkred")

prd=rrresults1.forecast(steps=len(test))[0]

prd = pd.Series(prd, index=test.index)

plt.plot(test.adj_close, label="Test Actual")

plt.plot(prd, label="Test Predicted")

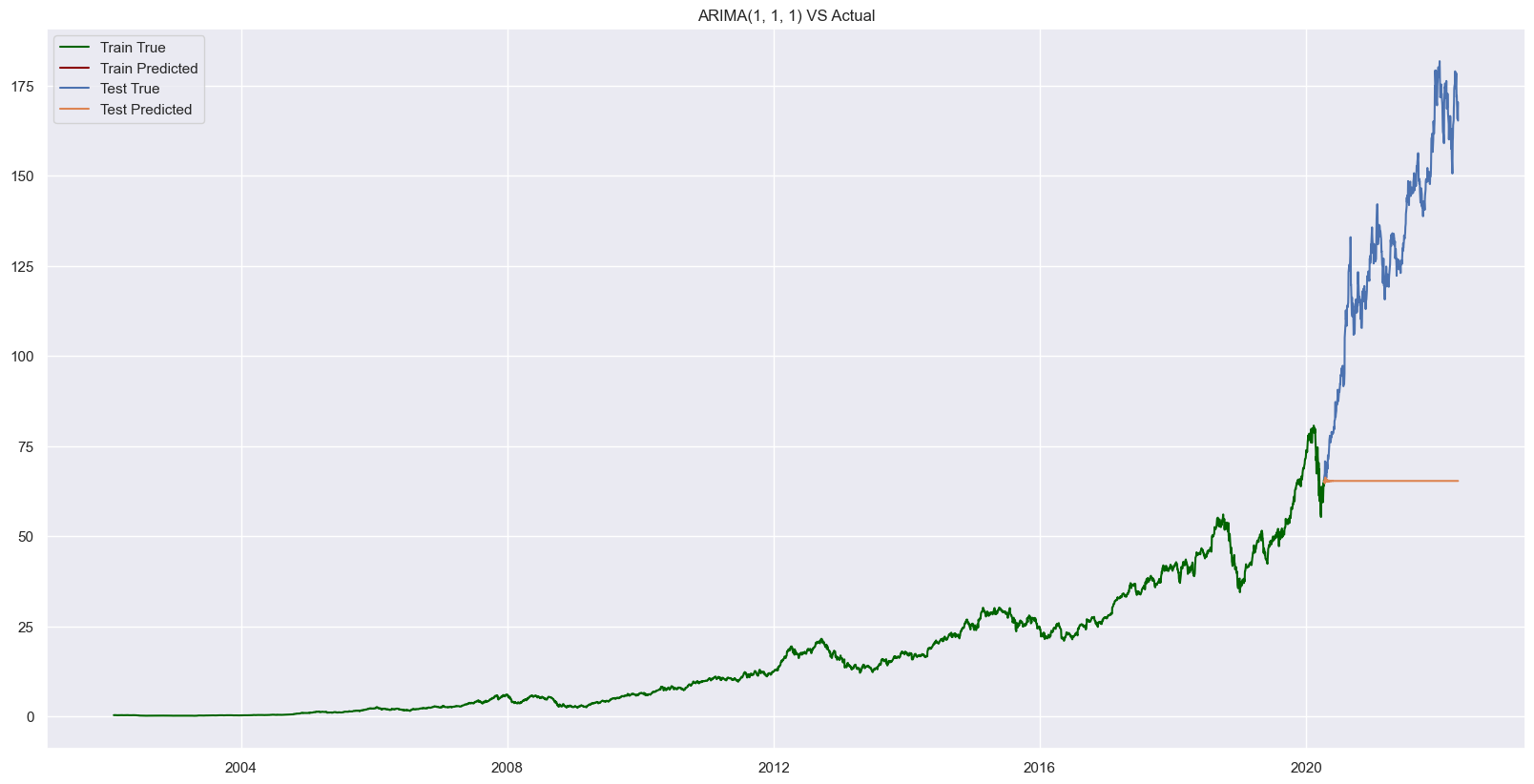

plt.title(f"ARIMA{best_order} VS Actual")

plt.legend(["Train True", "Train Predicted", "Test True", "Test Predicted"])

plt.show()

# plt.legend(loc='upper left', fontsize=15)

# plt.title(f"ARMA({(p,q)}) Value Performance")

percentage_change(fseries, train.adj_close), percentage_change(prd, test.adj_close)

(0.0, 0.03339882121807466)

Our ARIMA Model did not perform well in forecasting. Lets try to train a SARIMA Model.

Seasonal ARIMA (SARIMA)

Take seasonality when fitting a model. Use orders already found from previous steps. This model uses seasonal component also.

- SARIMA(p, d, q)(P, D, Q, M)

- D = 0 for stationary data, else the differencing value that makes data stationary.

- P from PACF and Q from ACF.

- The value of M should be chosen from Seasonal Decompose graph.

We know from the ARIMA that best order is (4,1,4) lets use that to find best seasonal parameters.

# check for weekly data

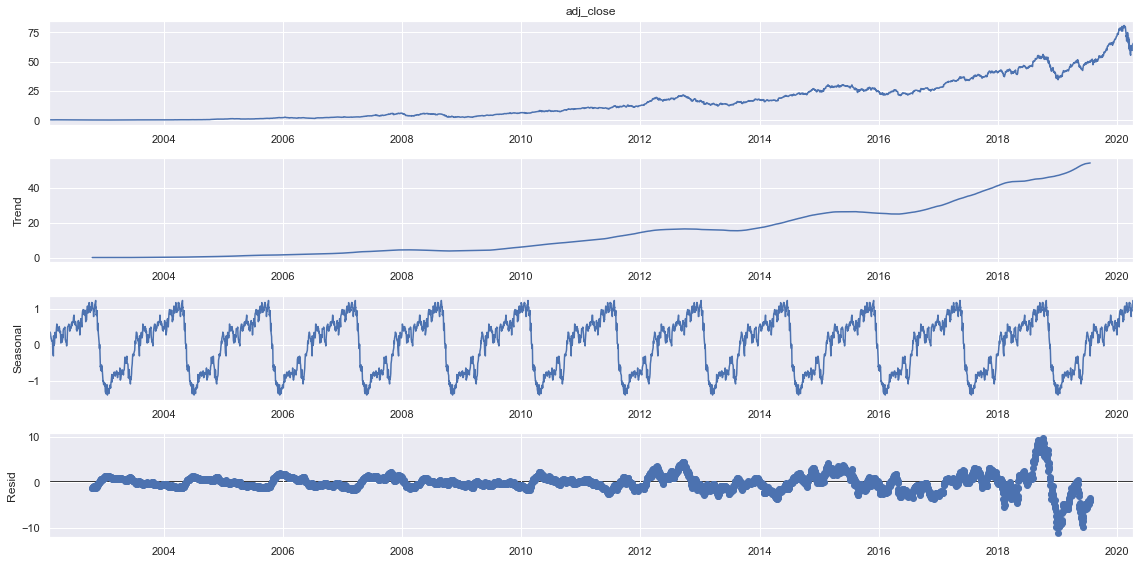

from statsmodels.tsa.seasonal import seasonal_decompose

sdec = seasonal_decompose(train.adj_close, model="additive", period=365)

sdec.plot()

plt.show()

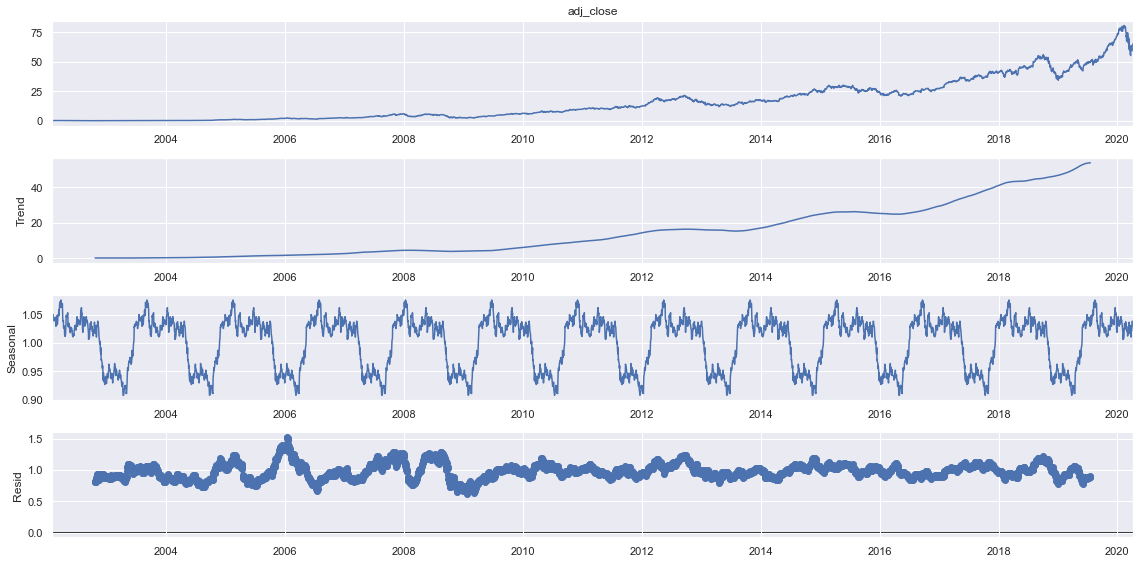

sdec = seasonal_decompose(train.adj_close, model="multiplicative", period=365)

sdec.plot()

plt.show()

from statsmodels.tsa.statespace.sarimax import SARIMAX

order = (4, 1, 4)

best_aic = np.inf

best_mdl = None

ms=[365]

best_order = None

best_sorder = None

for P in range(3):

for Q in range(3):

for D in range(3):

for m in ms:

try:

sorder = (P, D, Q, m)

# define a model

smodel = SARIMAX(train.adj_close, order=order, seasonal_order=sorder)

smodel = smodel.fit()

print(f"Order: {order}, Sorder: {sorder}, AIC: {smodel.aic}")

if smodel.aic<best_aic:

best_aic = smodel.aic

best_mdl = smodel

best_order = order

best_sorder = sorder

except Exception as e:

print(e)

# continue

print(f"Best Order: {best_order} Best SOrder: {best_sorder} AIC: {best_mdl.aic}")

Order: (4, 1, 4), Sorder: (0, 0, 0, 365), AIC: 5750.778071206555

---------------------------------------------------------------------------

KeyboardInterrupt Traceback (most recent call last)

KeyboardInterrupt:

It will take a lot time and will not even find best order. SO, lets use monthly average data instead of daily.

Using Monthly Average instead of Daily Data

import pmdarima as pm

mtrain=train.resample("1M").adj_close.mean()

mtest = test.resample("1M").adj_close.mean()

model=pm.auto_arima(mtrain, start_p=0, start_q=0,

max_p=5, max_q=5, m=12,

start_P=0, seasonal=True,stationary=False,

d=1, D=1, trace=True,

error_action='ignore', # don't want to know if an order does not work

suppress_warnings=True, maxiter=50)

Performing stepwise search to minimize aic

ARIMA(0,1,0)(0,1,1)[12] : AIC=inf, Time=0.47 sec

ARIMA(0,1,0)(0,1,0)[12] : AIC=982.844, Time=0.03 sec

ARIMA(1,1,0)(1,1,0)[12] : AIC=874.988, Time=0.28 sec

ARIMA(0,1,1)(0,1,1)[12] : AIC=inf, Time=0.83 sec

ARIMA(1,1,0)(0,1,0)[12] : AIC=946.930, Time=0.04 sec

ARIMA(1,1,0)(2,1,0)[12] : AIC=851.648, Time=0.37 sec

ARIMA(1,1,0)(2,1,1)[12] : AIC=830.994, Time=2.03 sec

ARIMA(1,1,0)(1,1,1)[12] : AIC=830.031, Time=0.31 sec

ARIMA(1,1,0)(0,1,1)[12] : AIC=inf, Time=0.61 sec

ARIMA(1,1,0)(1,1,2)[12] : AIC=830.257, Time=1.78 sec

ARIMA(1,1,0)(0,1,2)[12] : AIC=828.257, Time=0.73 sec

ARIMA(0,1,0)(0,1,2)[12] : AIC=841.816, Time=0.52 sec

ARIMA(2,1,0)(0,1,2)[12] : AIC=821.246, Time=1.01 sec

ARIMA(2,1,0)(0,1,1)[12] : AIC=inf, Time=0.90 sec

ARIMA(2,1,0)(1,1,2)[12] : AIC=823.234, Time=2.12 sec

ARIMA(2,1,0)(1,1,1)[12] : AIC=824.653, Time=0.59 sec

ARIMA(3,1,0)(0,1,2)[12] : AIC=822.891, Time=1.09 sec

ARIMA(2,1,1)(0,1,2)[12] : AIC=812.199, Time=2.64 sec

ARIMA(2,1,1)(0,1,1)[12] : AIC=inf, Time=0.83 sec

ARIMA(2,1,1)(1,1,2)[12] : AIC=814.068, Time=4.27 sec

ARIMA(2,1,1)(1,1,1)[12] : AIC=814.260, Time=1.52 sec

ARIMA(1,1,1)(0,1,2)[12] : AIC=811.256, Time=1.50 sec

ARIMA(1,1,1)(0,1,1)[12] : AIC=inf, Time=0.78 sec

ARIMA(1,1,1)(1,1,2)[12] : AIC=813.041, Time=2.93 sec

ARIMA(1,1,1)(1,1,1)[12] : AIC=813.519, Time=1.56 sec

ARIMA(0,1,1)(0,1,2)[12] : AIC=821.365, Time=1.25 sec

ARIMA(1,1,2)(0,1,2)[12] : AIC=811.824, Time=3.98 sec

ARIMA(0,1,2)(0,1,2)[12] : AIC=817.334, Time=1.53 sec

ARIMA(2,1,2)(0,1,2)[12] : AIC=815.090, Time=5.30 sec

ARIMA(1,1,1)(0,1,2)[12] intercept : AIC=808.813, Time=4.43 sec

ARIMA(1,1,1)(0,1,1)[12] intercept : AIC=inf, Time=2.13 sec

ARIMA(1,1,1)(1,1,2)[12] intercept : AIC=810.269, Time=5.39 sec

ARIMA(1,1,1)(1,1,1)[12] intercept : AIC=inf, Time=3.07 sec

ARIMA(0,1,1)(0,1,2)[12] intercept : AIC=820.084, Time=1.75 sec

ARIMA(1,1,0)(0,1,2)[12] intercept : AIC=827.189, Time=1.63 sec

ARIMA(2,1,1)(0,1,2)[12] intercept : AIC=810.401, Time=5.25 sec

ARIMA(1,1,2)(0,1,2)[12] intercept : AIC=815.022, Time=5.47 sec

ARIMA(0,1,0)(0,1,2)[12] intercept : AIC=838.364, Time=1.55 sec

ARIMA(0,1,2)(0,1,2)[12] intercept : AIC=813.281, Time=1.96 sec

ARIMA(2,1,0)(0,1,2)[12] intercept : AIC=817.661, Time=2.27 sec

ARIMA(2,1,2)(0,1,2)[12] intercept : AIC=inf, Time=8.56 sec

Best model: ARIMA(1,1,1)(0,1,2)[12] intercept

Total fit time: 85.290 seconds

# Forecast

n_periods = len(mtest)

fc, confint = model.predict(n_periods=n_periods, return_conf_int=True)

index_of_fc = mtest.index

# make series for plotting purpose

fc_series = pd.Series(fc, index=index_of_fc)

lower_series = pd.Series(confint[:, 0], index=index_of_fc)

upper_series = pd.Series(confint[:, 1], index=index_of_fc)

t = mtest

t.index = index_of_fc

# Plot

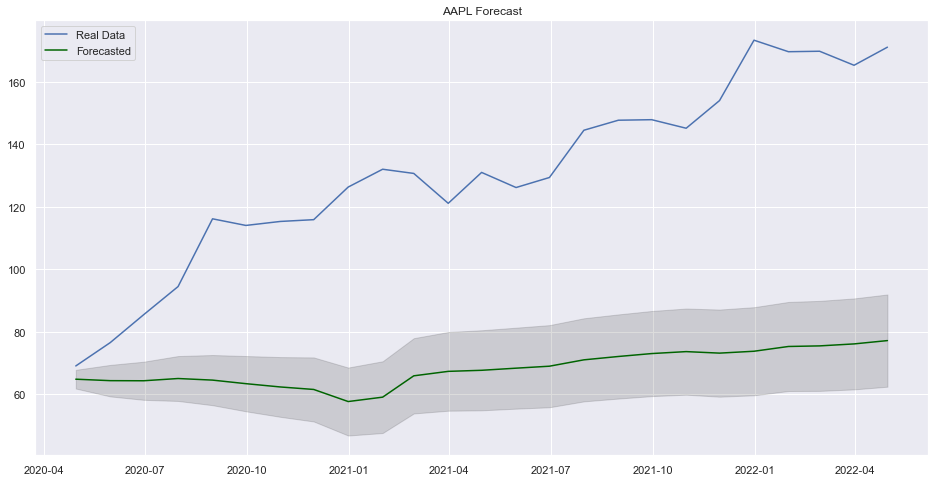

plt.plot(t)

plt.plot(fc_series, color='darkgreen')

plt.fill_between(lower_series.index,

lower_series,

upper_series,

color='k', alpha=.15)

plt.legend(["Real Data", "Forecasted"])

plt.title("AAPL Forecast")

plt.show()

Conclusion

It seems that our model was able to find some pattern in the test data but it is not near to be good. Using different level of date might be a best idea in this case.

Comments